The Earnings Picture

3rd Quarter results are mostly in. Reviewing this year's performance to date and looking ahead with lofty expectations for 2025 and 2026.

Earnings season is wrapping up across Wall Street and the quarterly results have been good, but not great, compared to recent averages. The financial data provider FactSet publishes a great public report weekly during quarterly earnings season breaking down the results. It can be found here: FactSet Earnings Insight and it’s the source for the highlights below.

The S&P 500 (with 95% of companies reported as of 11/22/24) have accomplished the following results for Q3 2024:

75% of S&P 500 companies beat EPS estimates (77% is the 5-year average)

61% beat revenue estimates (69% is the 10-year average)

On aggregate, companies beat EPS estimates by 4.5% (8.5% is the 5-year average).

They beat revenue estimates by 1.2% (2.0% is the 5-year average)

Overall EPS are set to grow 5.8% vs. the prior years 3rd quarter, the 5th consecutive quarter of year-over-year EPS growth.

So, while these numbers are decent and continue the growth of EPS, the outlook is much better than decent. Analysts are expecting an inflection in EPS that is driving a fair amount of today’s optimism in equity markets.

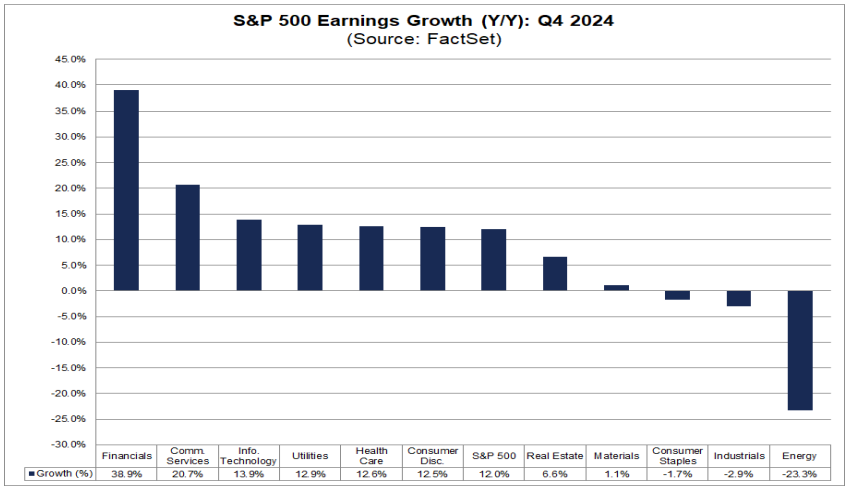

For the 4th Quarter 2024 (numbers that will be released early in 2025), the year-over-year EPS growth rate is expected to jump up to 12.0%. This rate of growth would be the highest since the 4th Quarter 2021.

FactSet breaks down the sources of higher growth:

6 sectors are expected to report double-digit earnings growth:

Financials (38.9%)

Communication Services (20.7%)

Information Technology (13.9%)

Utilities (12.9%)

Health Care (12.6%)

Consumer Discretionary (12.5%)

At the industry level, these 5 are the top contributors to growth: Banks, Semiconductors & Semiconductor Equipment, Pharmaceuticals, Interactive Media & Services and Broadline Retail.

This is evidence of the investment trends - from Artificial Intelligence (Tech/Comm Services) to datacenter power demands (Utilities) to GLP-1 weight loss drugs (Healthcare) - translating into tangible earnings growth for companies. Energy earnings are under pressure from lower oil and gas prices and tougher comparisons to a strong 2023 for the sector.

The momentum continues into 2025 with the following expectations for year-over-year EPS growth by quarter for the S&P 500:

Q1 2025: 12.7%

Q2 2025: 12.1%

Q3 2025: 15.3%

Q4 2025: 17.0%

This equates to the astounding 15.0% earnings growth expected in 2025. In 2026, analysts expect another 12.8%. In EPS for the S&P 500 index, this is $280.37/share in 2025 and $316.26/share in 2026.

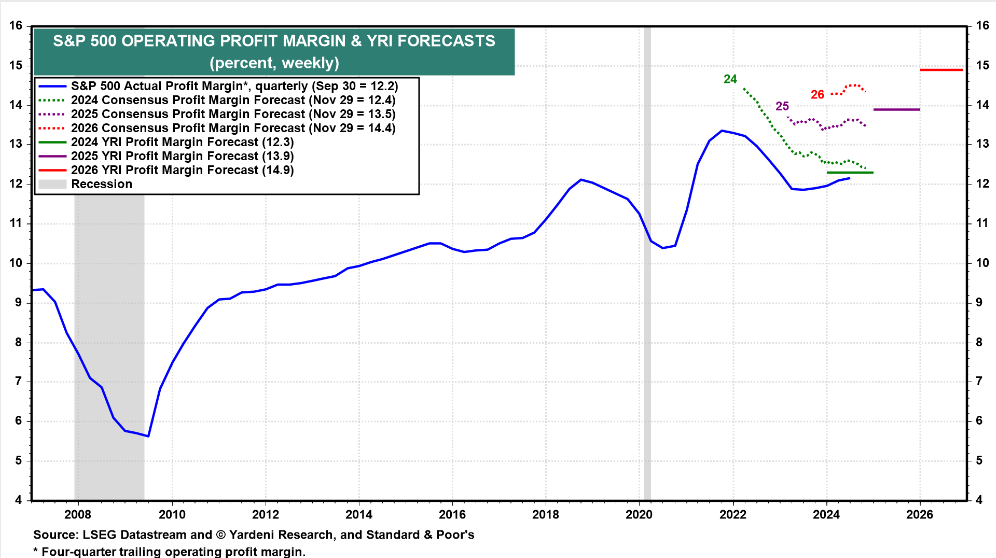

Higher earnings are driven by continued top-line growth; revenues are expected to grow by 5.7% in 2025 and 4.9% in 2026. But profit margins expanding to all-time highs is the primary catalyst of the earnings inflection. Profit margins (how much of sales is ultimately turned into profits) for the S&P 500 are expected to grow from 12.3% in 2024 to 13.9% in 2025 and 14.9% in 2026.

Rising profit margins are a signal of improved operational efficiency, strong pricing power and the structural advantages of companies in the index, specifically the mega-caps in the Technology, Communication Services and Consumer Discretionary sectors. All of these attributes contribute to the premium valuations seen in the market today.

In 2009, at the depths of the financial crisis, profit margins for the S&P 500 were a paltry 6.7% and has steadily risen as the the market has evolved. In 2009, the Technology sector made up 18% of the index where today it’s 31.3% and 37.3% if you add back Alphabet and Meta Platforms which are now placed in the Communication Services sector. As Technology’s weight in the index has increased, so has its contribution to the earnings of the index.

The earnings outlook for the S&P 500 reflects a strong trajectory of growth fueled by expanding profit margins, innovation, and continued operational efficiency from the companies within the index. We plan to post on the earnings outlook for the “rest” of the market in the coming weeks. Thank you for reading!

-John Nagle