Observations From the Market Reaction to Trump's Win

Trump's decisive victory has set off a flurry of activity in markets

The election has been called for Donald Trump and markets are moving in response.

In our view, it’s as simple as the election being conclusively decided (not held up with recounts and lawsuits), which is driving markets to rally. The market was likely to rally after the election either way if there was a clear winner as sentiment improved and volatility subsided.

Wall Street strategists are echoing this view and maintaining their outlooks, including this note from Goldman Sachs’ chief US equity strategist David Kostin:

"A key driver for stocks in the near term will be the reduction in political uncertainty, a dynamic that typically drives strong year-end returns in Presidential election years. Along with the resolution of election uncertainty, resilient recent economic growth data and continued Fed rate cuts support the healthy near-term outlook for U.S. stocks. We believe investors and corporate executives will now focus on four issues relating to the US equity market: (1) Post-election path of the S&P 500 index; (2) Equity investor positioning; (3) Rotations within the market, including those relating to trade and tax policy; and (4) The outlook for corporate M&A and IPO activity. We maintain our 12-month S&P 500 index target of 6300, reflecting a 9% gain from the current level."

The other piece of the narrative is a reboot of the 2016-2020 investing playbook under Trump, where ‘America First,’ pro-growth, domestic policies ignited markets in unique ways surprising market analysts who had discounted Trump’s chances of winning. Trump is generally viewed as pro-business and better for economic growth but also more inflationary and less deficit friendly. Globally, he is more of a protectionist in trade policy. The Senate has also been called for the Republicans, while the House is still uncertain but appears to be leaning that way as well.

These themes are percolating with the hyperreaction in the market today:

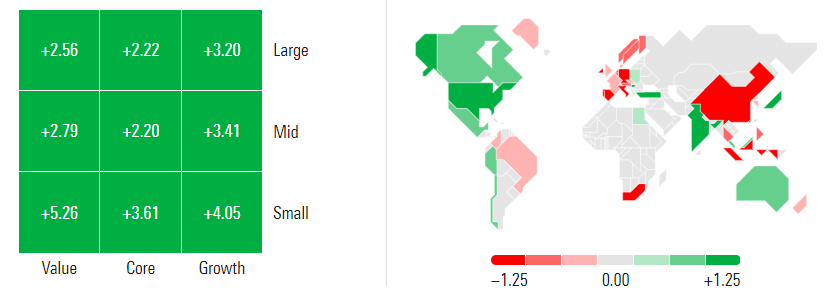

S&P 500 broke out to new all-time highs at the open and finished the day +2.53%. The Dow Jones Industrial Average gained over 1,500 points, up +3.57% on the day. The NASDAQ Composite was up +2.95%.

Small-caps saw even larger gains. The Russell 2000 was up +5.79% on the day. These companies are typically more domestic focused and have a heavy allocation to the Financials and Industrials sectors.

Financials are the best performing sector today in the S&P 500. Up +6.16%.

Regional Banks finished the day up +12.79%.

The largest money-center banks saw huge gains on the day:

The CBOE Volatility Index dropped from 20.49 on Tuesday evening to 16.31 today. This reflects less of an appetite to hedge risks in the market and is one of the largest single day declines in this volatility measure in the past 20 years.

The US Dollar Index is up +1.65% vs. a basket of global currencies in response to potential tariffs, deregulation and tax cuts which put a premium on dollar-denominated assets.

International stocks are not beneficiaries, these policies will theoretically hinder their ability to tap the American consumer and do business here. The MSCI EAFE and MSCI Emerging Markets indices were down -1.45% and -1.23% respectively.

Similarly, international bonds denominated in local currencies are under pressure because of the US Dollar strengthening.

Along with stocks, rates also spiked up although this is negative for current bondholders. The Bloomberg US Aggregate Bond Index fell -0.78% on the day.

Rising rates on the long end mean a steeper yield curve, generally indicative of economic health - but also signaling stickier inflation. 5-year inflation breakeven rates in the TIPS market are up to 2.46% after today. 5-year breakevens were at 1.86% in mid-September

The 10-year US Treasury yield rose to a high of 4.48% on the day and closed at 4.33%. The 10-year was under 3.6% in mid-September.

Other corners of the markets are also making interest moves:

Bitcoin is up +9.46% today. Trump is generally viewed as more favorable to crypto assets.

But, solar and green energy stocks are down on fears Trump will hamper clean energy progress and repeal the Inflation Reduction Act.

Whether any of these trends have staying power remains to be seen, the market is certainly prone to knee jerk reactions that could reverse at any moment but its a look into how investors are initially viewing a 2nd Trump term.

It’s worth reiterating we often noted leading up to the election, which is that the market performs over time regardless of who or what party is in office because its driven by an economy and earnings power that is not materially impacted by policy over the long-term. Certain industries and areas of the market may be better off than others given policy but for the market as a whole, its by and large inconsequential - which is why we’re glad to get it behind us and to return focus to the economy and fundamentals heading into year-end.

Speaking of those fundamentals, The Federal Reserve is also meeting this week and will likely announce a 0.25% rate cut tomorrow (11/7/24) afternoon. Following the announcement, Jay Powell will speak to the press and hopefully give us an idea of the FOMC’s plan for continued rate cuts and how the macro outlook changes with a new administration, if at all.

The views expressed herein are those of John Nagle on November 6th, 2024 and are subject to change at any time based on market or other conditions, as are statements of financial market trends, which are based on current market conditions. The information provided is for general informational purposes only and should not be considered an individualized recommendation of any particular security, strategy or investment product, and should not be construed as investment, legal or tax advice. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for a client's investment portfolio. All investment strategies have the potential for profit or loss and past performance does not ensure future results. Asset allocation and diversification do not ensure or guarantee better performance and cannot eliminate the risk of investment losses. The charts and graphs presented do not represent the performance of KCP or any of its advisory clients. Historical performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment management fee, the incurrence of which would have the effect of decreasing historical performance results. There can be no assurances that a client’s portfolio will match or outperform any particular benchmark. KCP makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based on information that KCP considers reliable, it is not guaranteed as to accuracy or completeness. This information may become outdated and KCP is not obligated to update any information or opinions contained herein. Articles herein may not necessarily reflect the investment position or the strategies of KCP. KCP is registered as an investment adviser and only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. Registration as an investment adviser does not constitute an endorsement of the firm by securities regulators nor does it indicate that the adviser has attained a particular level of skill or ability.